Public Trade Record

Real Trades

Real Results

Posted Every Week Since 2022

Not projections. Not simulations. The actual record — including the losing trades.

I know what numbers like these look like from the outside.

After 40 years in Financial Services, the last 28 as a Certified Financial Planner.

I sat across from people who had been shown "too good to be true" their entire lives.

And know exactly what triggers that reflex — and why it exists.

But I also know what it looks like when someone is 58 years old, behind on retirement, and quietly running out of time to fix it.

So before you look at a single number on this page, I want to say something that most people

in my position would never say: this system has losing trades. I'm going to show you those first.

Before You Look at a Single Number — One Thing Worth Knowing

This system runs on 20 minutes a day. After the market closes.

Not 20 minutes as a marketing number rounded down from two hours. Twenty minutes as the realistic outer limit of what an active trading evening requires — checklist open, conditions evaluated, trade placed or skipped, laptop closed.

Most evenings there is nothing to do at all.

That matters because the people this was built for are not sitting around waiting for something to do with their time. They are working, traveling, spending time with family, or figuring out what the next chapter looks like. A system that demands your days was never going to work for them. This one was specifically designed not to.

Twenty minutes. After hours. That's the commitment. Everything else on this page is about whether the results are worth it.

The Cleanest Public Record in This Space

Four years of open books. Here's what that means in practice.

Zero actions against this trading system or program — ever

Zero lawsuits

Zero student complaints about system integrity

Zero challenges to posted results since 2008

Zero actions against this trading system or program — ever

Zero lawsuits

Zero student complaints about system integrity

Zero challenges to posted results since 2008

Every trade posted publicly since 2022.

Nothing hidden. Nothing edited.

Transparency First

The Losing Trades —

Every One of Them

A system that claims perfection isn't a system. It's a pitch.

Here is every loss this system has produced since we began posting the public record in 2022:

2026 Corn — 5/12/26 $338 Loss

2026 Corn — 4/1/26 $387 Loss

2024 Bonds — 8/14/24 $656 Loss

2023 Corn — 3/9/23 $238 Loss

2023 Bonds — 9/5/23 $219 Loss

2023 Bonds — 11/29/23 $1094 Loss

2022 Bonds — 6/8/22 $875 Loss

Total Losing Trades Since 2022

7

Four years of

public record

Seven total losses

2025 had zero losing trades.

That is not typical — and I'm noting it here so no one expects it to repeat. One to four losses per year is the realistic range. That's the real record. That's what you're buying into.

What You're Looking at When You See This Record

Some weeks this system outperforms. Some weeks it sits out entirely. Occasionally since 2022 it had a losing trade and lost money in a week. Even with occasional losing trades, the system was never negative for any year.

All of it is posted.

I want to be clear about something most people in this industry never say: I could have made this record look better. There are weeks where sitting one day longer, or entering one day earlier, would have turned a flat week into a winning one. I didn't do that. The trades are posted as they happened, when they happened, with no adjustments made after the fact.

Why does that matter?

Because if you're invited to join this program, you're going to trade this system in real time — not in hindsight. You're going to have weeks where you sit out and wonder if you made the right call. You're going to have a loss at some point, probably within your first year. The record on this page doesn't hide any of that. It's exactly what you'll experience.

What the record does show is what a rules-based system looks like when the rules are followed consistently over years — through losing trades, through slow stretches, through markets that don't cooperate.

That's the point. Not perfection. Consistency under real conditions.

One to four losing trades per year is the realistic expectation going forward. 2025 had zero — and I've noted that clearly on this page because I don't want anyone expecting it to repeat. The system doesn't promise a clean year. It promises a documented process with capped risk and a record you can verify before you ever spend a dollar.

Simple Is Not a Limitation. It's the Whole Point.

There's a belief that's been sold to everyday investors for decades: that complexity is sophistication. That if something isn't hard to understand, it probably isn't worth trusting. That the people managing serious money must be doing something complicated — otherwise what are they being paid for?

That belief has cost a lot of people a lot of money.

After 40 years in financial services, here's what I know: the systems that hold up over time are not the ones that are hardest to explain. They're the ones that are hardest to break. Simple rules followed consistently beat complicated strategies executed inconsistently every time. Not sometimes. Every time.

This system trades two markets. It runs after hours. It caps risk on every trade. It sits out when conditions aren't right. That's it.

There is no dashboard to monitor all day. No news cycle to interpret. No gut feeling to second-guess. The checklist tells you what to do. You do it. You close the laptop.

If you were hoping for something more elaborate — this isn't it. But if you've spent years watching elaborate fail you, simple might be exactly what you've been looking for.

20 Minutes. After Hours. That's the Whole Time Commitment.

Not 20 minutes as a marketing number. 20 minutes as the actual outer limit of what this system requires on an active trading evening.

Most evenings there is nothing to do at all.

When there is a trade to evaluate, you open the checklist. You run through it. The conditions either meet the rules or they don't. If they do, you place the trade. If they don't, you close the laptop. Either way, your evening is yours.

No positions to monitor overnight. No pre-market scramble. No checking your phone during dinner to see what the market did. The trade is placed after hours, the result posts the next morning, and you move on.

That matters more than most people realize when they're first looking at this. It's not just about convenience. It's about sustainability. A system you can only follow when conditions are perfect is not a system — it's a hobby. This was built to run alongside a full life. Grandkids. Travel. Work you're not ready to walk away from yet. Whatever your next chapter looks like, 20 minutes after dinner fits inside it.

The trades are there. The record is there. The only question is whether you're ready to spend 20 minutes learning if this fits your situation.

How It Works

Why This Works —

The Boring Explanation

The results on this page are not the product of luck, genius, or a secret Wall Street loophole. They are the product of a simple, rule-based system applied to two physical commodities — consistently, after hours, with capped risk on every trade.

01

02

03

04

05

Two markets only

Not stocks. Not options. Not crypto. Two physical commodities with known, predictable behavior patterns that have held since 2008.

After hours only

Every trade happens after the market closes. Nothing disrupts your day.

Four days maximum in any trade

Never riding a position hoping it turns around. In and out. Done.

Sit out when conditions aren't right

A significant part of this system is knowing when not to trade. Some weeks, the correct decision is to do nothing. That discipline is what protects the record.

3–5% of capital at risk per trade. Maximum.

No trade is ever allowed to threaten the account. The math only works if the account survives.

Year-to-Date Results

This Year's Record —

Week by Week

Based on a $5,000 starting account. Every trade. Every result. No cherry-picking.

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

Short Window Retirement Planning Cash-Machine System

Short Window Retirement Planning Cash Machine System. Less Risk. Fewer Days in the Market and Higher Profit than the Dow Every Year since 2008. 20 Minutes a day After market hours.

You won't see a risk reward ratio here. SWRP uses a different framework. Every trade has a predetermined profit target and a predetermined stop loss set before the trade is placed. The win rate above measures how often the profit target gets hit. The losses are capped at 3 to 5 percent of account value per trade.

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

Retirement Isn't Optional...

Controlling and Enjoying It Is!

What Makes This System Different

-

Side-by-Side Results That Matter

We started this year with two identical $5,000 accounts:

• One followed the Dow (now worth $)

• One followed this system (now worth $)

One followed headlines. The other followed a plan. -

Built to Minimize Worry

✓ Small, limited risk (3–5% at most)

✓ In and out in under 4 days

✓ Runs after hours in under 20 minutes — so your days stay completely yours -

Designed for People Over 50 Who Are Done Guessing

This isn't for traders. It's for people who want:

• A rules-based process they can follow without a finance degree

• To stop watching their savings erode and feel powerless about it

• More time with family, not more screen time

• Control over their next chapter — on their own terms

Dr. Fred Rouse on Wall Street Today — helping everyday people take back control of their financial future.

Featured in Forbes Forecasts & Strategies — a retirement income system built for real people, and proven to work.

As seen on NewsChannel 10 — featured for helping thousands of pre-retirees take control of their financial future.

As Featured In...

About Dr. Fred Rouse

Dr. Fred Rouse spent 40 years in Financial Services, the last 28 as a Certified Financial Planner, before building this system. He holds a PhD in Taxation and a DBA, and is a U.S. Coast Guard and Army National Guard veteran.

But after decades watching clients lose money and sleep over Wall Street’s ups and downs, he stepped away from the mainstream to build something different.

He watched too many good people do everything right and still end up short. That bothered him enough to spend ten years and $350,000 of his own money building a system that didn't require them to trust Wall Street at all.

The result? A simple, proven system designed for real people — especially those 50 and older — who want safe, after-hours income without risking their retirement.

Dr. Fred has been featured in NBC, CBS, Fox, and MarketWatch, and co-authored bestselling books with names like Jack Canfield and Brian Tracy. But he’s most proud of helping everyday folks finally feel confident, independent, and in control of their financial future.

About Dr. Fred Rouse: DrRouseNow.com/AboutDrFredRouse/

Dr. Fred Rouse is an international and nine-time best-selling author who’s written alongside Jack Canfield (Chicken Soup for the Soul), Brian Tracy (Cracking the Code to Success), Dick Vitale (Never Give Up), and Lisa Nichols (Rise Up).

But the work he’s proudest of? Helping everyday people create reliable income and a real retirement — without fear, confusion, or Wall Street risk.

This Changed everything for us...

"Dr. Rouse's program, completely changed our lives."

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

I was reflecting on my path to become a trader for short term retirement since it's been well over a year since I began down this path. I can say with the utmost

certainty that I would not be earning the profit I am now earning without your course and probably would have given up at some point like most do.

Bill Simons

Graduate Student

Corn Trades: Real Income, Real Impact

- Total Collected: $

- Evenings Active:

- Win Rate: 100%

How This Could Strengthen Your Retirement:

- 3 Contracts: $ — Enough for 3 months of travel

- 5 Contracts: $ — Or 6 months of healthcare costs

These aren’t lucky guesses.

Every result followed the same checklist I’ve refined since 2008 — and that you'll use too.

Click the Corn Chart below to see EACH Detailed Trade

My only regret is not finding out about Dr. Rouse's Quiet Trader program before I wasted my time and money on other programs that didn't live up to their hype!

Randolf Babbit

The information in this course weeded out the unnecessary information I already knew and left me with a greater understanding of what is important to use to trade profitably.

I feel like I have a greater understanding of how to trade without spending all day to do it and make a consistent profit at trading commodities.

The process to trade this way is simple and straight forward. It doesn't take a lot of time. If done properly and the rules are adhered to the profits will come.

My only regret is not finding out about Dr. Rouse's Quiet Trader program before I wasted my time and money on other programs that didn't live up to their hype!

"Dr. Rouse's program delivered such great results, I told my 60 yr old son to take it too"

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

Bond Trades: Consistent Cash Flow You Can Count On

- Total Collected: $

- Evenings Active:

- Win Rate: 100%

How This Could Strengthen Your Financial Base:

- 3 Contracts: $ — Covers 6 months of groceries

- 5 Contracts: $ — Pays a full year of property taxes

No stock market exposure.

This part of the system runs calmly in the background — so your money grows, even when Wall Street doesn’t.

Click the Bond Chart below to see EACH Detailed Trade

I owe Dr. Fred Rouse a huge THANK YOU! The Quiet Trader program delivered everything I expected. I am 3 years in now. I followed the program as closely as I could without trying to speed through it. I made my first trade 7 months into studying the chapters and doing back and forward testing. What I have found is that when I follow the program exactly, I come out on top.

JIm Blancet

Graduate Student

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

Watch Bob Guiney interview Dr. Fred Rouse about how his system

is transforming lives and helping people achieve financial freedom.

"The Risk Comparison — Same Period, Same Capital

$5,000 Invested • Here's what it is Year-to-Date

- ▼ $

- ▼ Days in the Market

- ▼ 3x More Risk, Zero Peace of Mind

You worked too hard to spend retirement riding waves you can’t control.

Bob Guiney on why this system is different from everything else he's seen.

6 Weeks in the RED this year.

Market Reality Check

▲ $

Year to Date System Total

$

$

Year to Date Dow Total

A Major Dow Drop Wipes Out Years of Gains

- • A $5K Dow Investment Can Lose $500+ in a Single Drop

- • Recovering Losses Gets Harder as Drops Get Bigger:

- - A $1,000 loss needs $1,250 gain just to break even

- - A $2,200 loss? You’d need nearly $4,000 back

According to MarketWatch, 92% of people working past traditional retirement age say they need more income. This system was built specifically for that situation.

What the Bank Paid You While This System Was Running

Since 2022 — the same period covered by this public trade record — the FDIC national average savings account interest rate has fluctuated between roughly 0.06% and 0.61% per year. As of early 2026 it sits at 0.39%.

That is not a typo.

On a $5,000 account, here is what those numbers actually produce:

At 0.06% — $3 per year. Enough for a cup of coffee. At 0.39% — $19.50 per year. Enough for half a tank of gas. At 0.61% — $30.50 per year. A decent dinner out, once.

The bank is not a villain. It is doing exactly what it is designed to do — hold your money safely and pay you as little as possible to do it. That is a reasonable trade when you are 30 years old and time is on your side.

It is a different trade entirely when you are 55, 60, or 65 and the window is short.

The comparison that matters is not between a savings account and a riskier investment. It is between doing something disciplined and proven with a portion of your capital versus letting it sit while inflation quietly does the math against you.

The posted trade record on this page covers the same years. The numbers are there. The bank's numbers are there too, published monthly by the FDIC. You can look up both.

One of them changes your retirement. The other buys you dinner once a year.

Source: FDIC National Average Savings Rate, 2022-2026. Current rate as of February 2026: 0.39% APY. Past system results are not a guarantee of future performance.

Four Years of Public Record — Verify Any Year

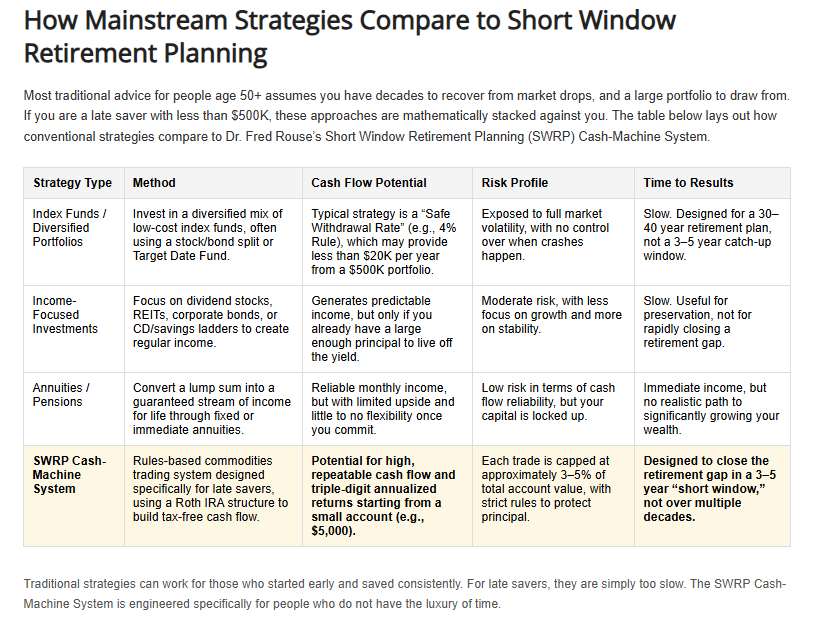

How Mainstream Strategies Compare to Short Window Retirement Planning

Most traditional advice for people age 50+ assumes you have decades to recover from market drops, and a large portfolio to draw from. If you are a late saver with less than $500K, these approaches are mathematically stacked against you. The table below lays out how conventional strategies compare to Dr. Fred Rouse’s Short Window Retirement Planning (SWRP) Cash-Machine System.

| Strategy Type | Method | Cash Flow Potential | Risk Profile | Time to Results |

|---|---|---|---|---|

| Index Funds / Diversified Portfolios | Invest in a diversified mix of low-cost index funds, often using a stock/bond split or Target Date Fund. | Typical strategy is a “Safe Withdrawal Rate” (e.g., 4% Rule), which may provide less than $20K per year from a $500K portfolio. | Exposed to full market volatility, with no control over when crashes happen. | Slow. Designed for a 30–40 year retirement plan, not a 3–5 year catch-up window. |

| Income-Focused Investments | Focus on dividend stocks, REITs, corporate bonds, or CD/savings ladders to create regular income. | Generates predictable income, but only if you already have a large enough principal to live off the yield. | Moderate risk, with less focus on growth and more on stability. | Slow. Useful for preservation, not for rapidly closing a retirement gap. |

| Annuities / Pensions | Convert a lump sum into a guaranteed stream of income for life through fixed or immediate annuities. | Reliable monthly income, but with limited upside and little to no flexibility once you commit. | Low risk in terms of cash flow reliability, but your capital is locked up. | Immediate income, but no realistic path to significantly growing your wealth. |

| SWRP Cash-Machine System | Rules-based commodities trading system designed specifically for late savers, using a self-directed Roth IRA structure where qualified distributions are tax-free. | Aims to produce cash flow you control from a small account. Every trade since 2022, wins and losses, is posted publicly at DrRouseNow.com/trades so you can judge the real record yourself. | Risk is defined in advance on every trade, typically about 3–5% of the account, and the system runs on a small, separately funded amount so the rest of your savings stays untouched. | Designed to build a supplemental income stream you control over a short window of a few years, rather than a multi-decade plan. |

Traditional strategies can work for those who started early and saved consistently. For late savers, they are simply too slow. The SWRP Cash-Machine System is engineered specifically for people who do not have the luxury of time.

How This System Compares to Professionally Managed Commodity Trading

Striker Securities has published real-time performance rankings for commodity trading systems since 1991. Their rankings at Striker.com/ranking.php draw from approximately 200 systems and include commissions and fees. They are updated daily and publicly available to anyone.

As of this writing, the top-performing system in the under $10,000 account category over the past year produced $15,880. The top performer in the $10,000 to $19,999 category produced $18,013.

This system produced $32,956 over the same period on a $5,000 starting account.

Three things that comparison does not show on its own.

First — Striker's own disclaimer states their rankings may not reflect losses those systems experienced during the period. Every losing trade this system has produced since 2022 is listed at the top of this page. Nothing is hidden.

Second — the Striker systems in the under $10,000 category require accounts of up to $9,999. This system starts at $5,000.

Third — those are managed systems. Someone else is trading your money. This system is traded by you, on your schedule, after hours, using a time-tested process and checklist that takes under 20 minutes.

You can verify their current rankings at Striker.com/ranking.php at any time. The comparison above will change as their rankings update. What will not change is the five-year record posted on this page — or the fact that this system has outperformed their top-ranked systems in every year of that record.

1. SWRP vs. Every Major Alternative

| Criteria | SWRP | Traditional Retirement Planning | Annuities | Real Estate | Trading / Options Programs | Index & Market Strategies |

|---|---|---|---|---|---|---|

| Designed for Late Savers (50+ with < $500K) | Yes |

No No |

No |

No |

No |

No |

| Core Savings Not Exposed to Market Loss | Yes |

Sometimes Sometimes |

Yes |

No |

No |

No |

| Produces Income in 3–5 Years | Yes |

No |

No |

Maybe |

No |

No |

| Risk Defined in Advance on Every Trade | Yes |

No |

Yes |

No |

No |

No |

| Rules-Based, No Market Predictions | Yes |

No |

Yes |

No |

No |

No |

| Requires No Specialized Skills | Yes |

Yes |

Yes |

No |

No |

Yes |

| Tax-Free Income Potential (Qualified Roth) | Yes |

No |

No |

No |

No |

No |

| Mandatory Forward-Testing | Yes |

No |

No |

No |

No |

No |

| Fully Public, Verifiable Record | Yes |

Mixed |

Mixed |

No |

No |

Mixed |

| Built to Produce Ongoing Cash Flow | Yes |

No |

Sometimes |

No |

No |

No |

| Emotional Stress Level | Low |

Medium |

Medium |

High |

Very High |

Medium |

| Overall Suitability for Late Savers | Highest |

Low |

Low–Medium |

Low |

Very Low |

Low |

2. SWRP vs. Commodity Trading Alternatives

| Criteria | SWRP | Retail Futures Systems | CTA Managed Systems | Algo Systems Online |

|---|---|---|---|---|

| Designed for Retirement Income | ✓ Yes | ✗ No | ✗ No | ✗ No |

| Losing Trades Per Year | ✓ 1 to 4 | ✗ 20 to 40 | ✗ 30 to 50 | ✗ 20 to 60 |

| Time Required Per Day | ✓ Under 20 Minutes | ✗ 1 to 3 Hours | △ None — Managed | ✗ 1 to 2 Hours |

| Minimum Starting Capital | ✓ $5,000 | ✗ $10,000 Plus | ✗ $250,000 Plus | △ $5,000 to $50,000 |

| Your Money Stays in Your Account | ✓ Yes | ✓ Yes | ✗ No — Managed | ✓ Yes |

| Public Trade Record Posted | ✓ Yes — Since 2022 | ✗ No | ✗ No | ✗ No |

| Independent AI Verification | ✓ Yes | ✗ No | ✗ No | ✗ No |

| Stock Market Exposure | ✓ None | ✗ High | ✗ High | ✗ High |

| Risk Per Trade | ✓ 3 to 5% Defined | ✗ High and Variable | ✗ 10 to 30% Drawdowns | ✗ High and Variable |

| Maximum Days in Any Trade | ✓ 4 Days | ✗ Varies — Often Weeks | ✗ Varies — Often Months | ✗ Varies |

| Emotional Stress Level | ✓ Low | ✗ Very High | △ Medium | ✗ High |

| Overall Suitability for Late Savers | ✓ Highest | ✗ Very Low | ✗ Low | ✗ Very Low |

The AI verification is posted at DrRouseNow.com/ai-swrp-review. The trade record is posted on this page DrRouseNow.com/trades.

No other system in any of these categories can make either statement.

What the Comparison Makes Clear

There is no other commodity-based system designed specifically for retirement income. Every alternative in this category was built for speculation, not for predictable monthly cash flow in a short window.

Every other system fails in at least one critical area for late savers. Too much capital required. Too much time required. Too much risk. No public record. No independent verification.

SWRP is the only system in this category with a public trade record posted weekly since 2022, independently verified by AI, with risk capped on every trade and no stock market exposure.

This System (Jan 2022 – Dec 2023)

$109,200

Total Profit on $5K

Dow Jones (Jan 2022 – Dec 2023)

$720

Total Profit on $5K

The Reality: The Dow surged in 2024 — but from Jan 2022 to Dec 2023, it delivered just $720 total. That’s only 7% per year.

It's inconceivable to live on $720 for 2 years with inflation. Yet $109,200 (your system's profit) changes everything.

-

Traditional planning fails because percentages lie:

A 1-point Dow move = $10 REAL dollars - The 10/13/22 crash tanked the Dow over 30% — enough to erase years of retirement gains

- 92% of late retirees (MarketWatch) need more income — this system solves that

You can't pay bills with percentages. You need REAL tax-free income. See the Previous Year's Posted Trades

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

This comparison was independently reviewed by AI to confirm accuracy and suitability for late savers.

Why These Trade Results Look Different From Anything You've Seen

Most retirement strategies were never designed for people over 50 who are behind and running out of time. They rely on slow growth, market timing, or large account balances. SWRP is engineered for a completely different purpose — predictable, protected cash flow and in a short 3–5 year window.

Traditional strategies can work for early savers. But for late savers, they are simply too slow. SWRP is built for people who need results in years, not decades — under their control, with capped risk, no leverage, and no predictions.

Who this program is actually built for — in 37 seconds.

Why Financial Planners Hate This Man's Retirement Method

If you've ever been told your situation is "too late to fix"... this is the conversation you should have heard years ago.

Jack Canfield Recommends Dr. Fred Rouse’s Proven System for Financial Freedom

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

There Are Only Two Kinds of People Who Land on This Page

The first kind has known for a while that something needs to change. They've run the numbers. They've done the math on what Social Security actually pays. They've looked at their savings balance and felt that quiet unease that shows up around 2am. They're not in denial. They just haven't found something they trust enough to act on yet.

The second kind has known all of that too. For longer. And they're still waiting for the right moment. When the market settles. When things are less busy. When they feel more ready.

Here's what 40 years in financial services taught me about the second group: the moment never comes. Not because they're lazy or careless. But because waiting feels safer than deciding. And every month that passes, the math gets a little harder and the window gets a little shorter.

I'm not going to tell you which one you are. You already know.

What I will tell you is this: the people who get the most out of this system are not the ones who felt the most confident when they started. They're the ones who decided that where they were headed without a plan was scarier than learning a new one.

If that's you — the next section is worth reading carefully.

Lisa Nichols — co-author with Dr. Rouse on Rise Up*,

and one of the most recognized personal finance voices in America.

Is This Really Right for You?

You're over 50, want more control over your money, and are looking for a safe, no-hype system you can use in just 20 minutes a day. You're done with stock market stress, and you're ready for something real. If that sounds like you — this could be your breakthrough.

- ✓ A rules-based process you can follow — no finance degree required

- ✓ Clear steps, simple rules, and full control over your own account

- ✓ No day-trading, no crypto, no screens during the day

- ✓ Built specifically for people 50+ with no prior trading experience

Do most of these sound like you?

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

You've seen the record. You know where you are.

Retirement isn't optional — controlling it is.

Want to understand how this works before you apply?

See how we help clients — DrRouseNow.com/HowWeHelp

And why choose Dr. Fred — DrRouseNow.com/WhyDrFred

"Dr. Fred actually cares." — Zack Viscomi, SWRP Graduate